How to Bring a Billion People to Crypto: Argent's Itamar Lesuisse

The key is they shouldn't have to know it's crypto.

Good morning defiers! I spoke with Itamar Lesuisse, co-founder of Argent, a smart-contract based crypto wallet. Argent has made great strides in simplifying the experience of using crypto and DeFi products. They integrated with MakerDAO a few weeks ago, allowing users to open a CDP in a couple of taps, and last week they integrated with Compound Finance, to make it easy to start gaining interest on savings.

Itamar talks about the decisions he and his team have made along the way to make their wallet act more like a traditional bank account, and about the Maker and Compound integration. He also talks about what’s next: A fiat on-ramp (likely with Wyre in the U.S.) to be announced in the next couple of months, account insurance next year, and crypto wallets to manage identity.

The interview has been edited for clarity and brevity and I’ve bolded my favorite quotes.

Camila Russo: Give me the quick background on you and your team,

Itamar Lesuisse: We're three engineers and I worked as a product manager in the early days at Amazon, and I worked on payments at Visa, so I already knew very well the payments space before crypto. And then had a few start ups. My last startup was the most successful. We were the largest mobile brain training application, called Peak. It had 60 million users running a very large subscription business. So we knew the consumer space extremely well. Gerald our CTO, was my co-founder at Peak. And the third co-founder, Julian, comes from a more security and cryptography background. And so we had that team from day one that was really a consumer centric and the ability to work at across the tech stack.

CR: How did you get into crypto?

IL: My co-founders and I started looking at crypto from a technical perspective, and then at some point when I made my first transfer and I just felt the magic. But then realized that building a consumer product like a dapp would be too early because the way people interact with that space was not yet where it should be and we started thinking about how to solve all that friction. A user should not know he's interacting with a block chain. All the complexity has to be abstracted.

CR: When was this, what, what transfer? What was it just like you, the first time you bought bitcoin or exactly how did that happen?

IL: So it was a weird situation. This was two and a half years ago and we had sold our company, Peak, and we had the big issue around payment. Basically, the bank made a mistake and froze the transfer. It was a U.S. dollar payment and for a few weeks the money didn't arrive. It was a nightmare. I had no cash, no money at the time. When I finally got the money and I bought ETH. I was tracking the transfer from Kraken to my hardware wallet, and the ability to see that transaction, knowing that there was just no one in the middle and at the time it was free, the transfer was less than a cent. It took, you know, 15 seconds. I would say that was it. My co-founders at Argent Gerald and Julian were looking at blockchain from a technology perspective for already a year, but that's really the first time I got it.

CR: Was that when you decided to start Argent?

IL: I would say really Julian started working around August, September, 2017 on a prototype. In summer 2017 We had the idea, we had the idea to really re-think the old model of how do you own the assets and also interact with a protocol and dapps. So that was the starting point. And then Gerald and I, when we were done with our transition from the old company to the new one, we joined him.

CR: What were the main goals of Argent starting out?

IL: Blockchain redefines ownership, redefines the ability to move value. And for us it's a new layer on top of the current web. Will it be a fully new decentralized web? Who knows? But for us it's a new layer that should be part of the web we use every day. That will just have a huge potential. And so we started with the idea that people should have ownership of their money, their identity, their data. And so we spent a lot of energy and research really on re-thinking what is a wallet? The wallet is basically a private key in a different package. We thought that's not the right way. Look at the wallet in your pocket, if you lose it, you lost it. Someone steals it they have your cash. So you can think of argent more as a bank account, but that is fully decentralized and non-custodial.

Users understand and are comfortable with their bank because you can always recover your password, your funds, and block transaction that are fraudulent. You don't worry about transaction fee or gas fees or complex stuff. So we built our journey with that in mind. It's abstracting all the complexity. Starting with no post-it with 12 or 24 words on it. We want to bring a billion people to crypto, but they don't need to know that it's crypto. That's our view.

CR: So if you could kind of summarize the things that you did to get there. What are the main things that differentiate you from most of the other wallets to make this experience easier?

IL: Step one from a technical perspective, what we did, we moved security to the smart contract layer. Your funds are stored in a smart contract, which allows us really to add logic. The first logic we added is recovery. With Argent you don't back up a seed phrase. It's okay to lose your key because we have recovery mechanisms that rely on what we call guardians. That was really the first big starting point because guardians can be friends and family, or it an be your own hardware wallets, or it can be a service, someone you trust to take that role. And it's exactly the experience of your bank. You lose your phone, you call your guardian, freeze your wallet, and then you get the new phone and the guardian gives you access. That's really an experience people understand. That was the starting point. So no more seed phrase.

After that, we looked at every other element of friction. So gas. Too complicated. Users don't have to pay gas. We use what you call meta transaction. So your phone is only signing an intent and we relay that to the blockchain and it can be paid in any currency, doesn't have to be ETH. But right now we subsidize it. Now you can start sending Dai, you can do things without worrying about the complexity of gas.

Then we added a lot more elements of security. You can literally take my phone, send all the ETH on my account to you, but the smart contract will lock that transfer. It will see a large transfer to an untrusted address and it will take 24 hours to go through. So you have 24 hours to cancel it and again, that's very similar to your bank, which would call you if there's a suspicious transfer. So really making the best, most secure place, but without complex interactions with multisig.

CR: What's the transaction limit before it gets blocked?

IL: The user decides the limit and then they can decide to trust certain addresses and you can send to those addresses as much money and as often as I want.

CR: Going forward, what other services do you expect to add? Do you expect it to function as a full bank with, with lending and borrowing and trading and all of that or keep it simple?

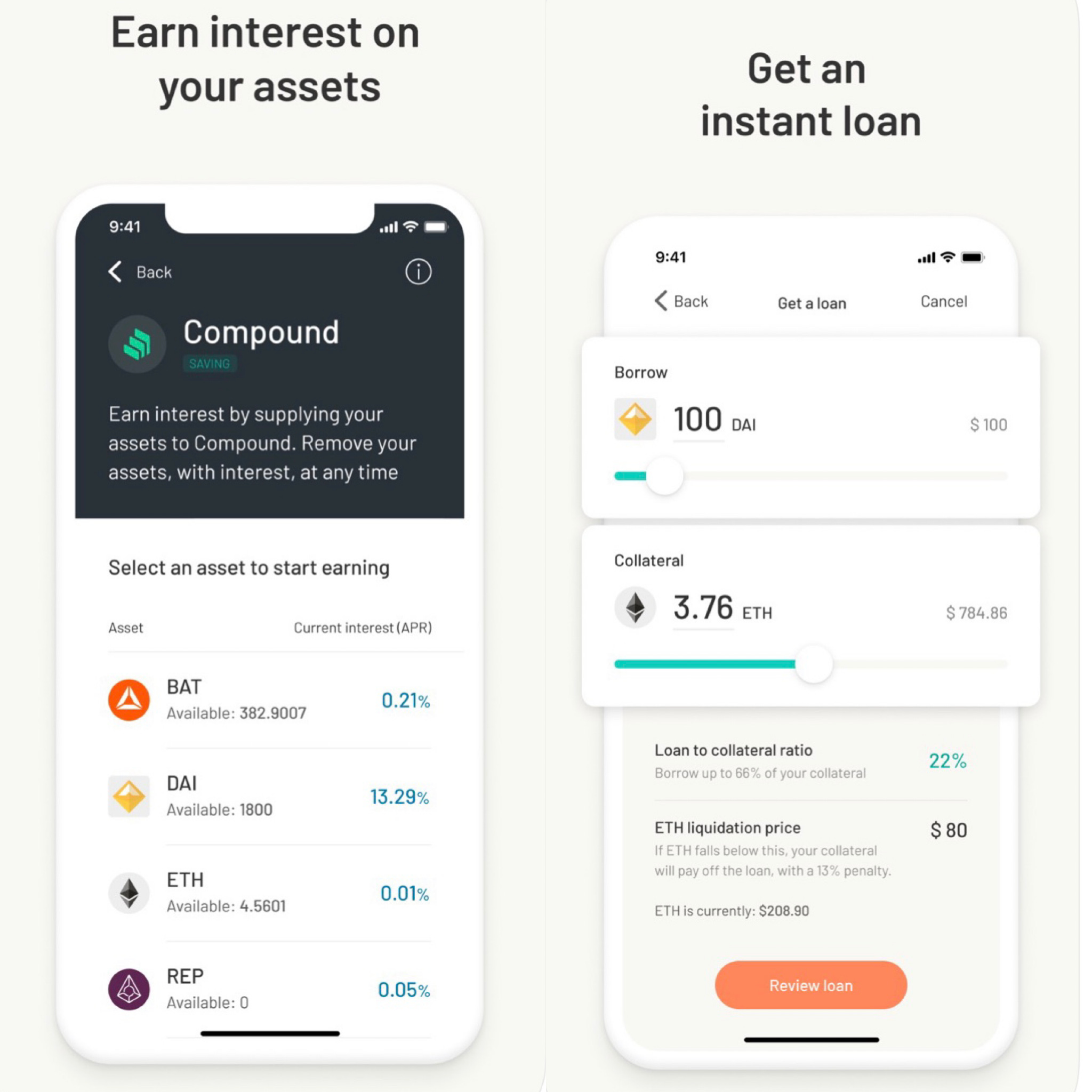

IL: This is step one for us. We had the basic wallet which is secure, easy to use, but actually that's pretty useless. So I have a place where you can send, receive crypto. For us it's not about that. It's really bringing a new type of service for a billion users. So we started working on use cases. So not only with a decentralized exchange, which we think is still a niche use case. But where we think it gets more interesting, is for example when we added Maker. So we turned something that is extremely complex, opening a CDP [collateralized debt position], five to seven transactions, to one tap on your phone and it's already happening. You pick an amount to tap a button, you open your borrowed Dai on Maker. The reason we can do that is because you have a wallet that has logic in it that can orchestrate, that it's programmable money. Normal wallets are not programmable money. We are programmable money because your wallet can be programmed.

The next exciting integration is Compound. Earning interest. So you go in your account, you push on the button, you say, I want to save $1,000, and you can make 10% interest on that. I mean it took me three seconds to open a Dai savings account and if we wait 30 seconds or a minute, you'll start to see the amount increasing, as you earn interest. So that's where it gets really interesting. We are also working on the long run for users to be able to go from dollars to crypto on Argent. And then you have a product that someone who doesn't understand crypto can download.

Image source: Argent’s App Store preview

CR: But you will still have to buy Dai first to start earning interest right? You’re not going directly from the thousand dollars to gaining interest?

IL: Yes. But then what we're doing is we're integrating the on-ramp ability. So you will be in Argent, you will say top up my account with $1,000 and then you start saving. So that's the next step that will come in the next two months.

CR: Which on-ramps are you considering?

IL: So we're talking to all the big players globally. In the U.S., Wyre is an obvious one that many people are working with, so we're working with them. There will be a first integration very soon. And then they are developing new features to really make that a better experience.

CR: And to connect with bank accounts in the U.S., are there any regulatory issues that you have to deal with?

IL: Because we work with a third party, we don't have the regulatory burden. That's really the reason to work with someone like Wyre. They’re the ones who do KYC, AML. Technically they're the ones linking the bank account and accepting payment, and we stay fully non-custodial.

CR: It's really interesting to be able to cut down the number of steps that users have to take from like having a dollar in your bank account to like earning interest on a DeFi platform. But there's also risks in doing that. Maybe if like people don't realize that they're actually holding crypto and that these platforms are new and risky. How do you strike the right balance? Because I the same thing happens with the CDP. You're making it easy, but at the same time there's a high risk with liquidation and all of that.

IL: They’re two very different risks. With the CDP yeah, it's really a financial risk, the liquidation. If you don't put enough in collateral, you’ll see a red symbol and we show you when you’re getting too close to the liquidation. Also, people who are using that product are already knowledgeable. You have no reason to open a CDP if you're just a casual user. For Compound, the risk a little bit less financial, there's much less counterparty risk. It's not like you're lending based on the credit score, there have been audits, but the risk is that overall this is quite a new technology.

So step one, the answer to your question is to be transparent and make sure the user know the risk they’re taking. We don't believe we will get straight away a billion people that don't know anything about crypto. But the long term solution is really insurance. So we want to insure accounts. That's something for 2020 that were really set on doing because then we can really match a bank’s value proposition.

CR: That’s super interesting. Are you considering Nexus Mutual?

IL: We are talking to them. Right now the platform is a bit too young to cover all of our accounts. You can only cover 700 ETH total. That's not enough. So the idea is to run a pilot, see how it works, what impact it has on user behavior, and then wait for them to grow. So as the Nexus Mutual grows, they'll be able to cover more. And then we are also talking to traditional insurers.

CR: Also wanted to ask you about the approach that MetaMask is taking with their wallet. They recently launched the mobile app and where they're trying to become more of a browser of dapps. Is that something you'd want to add to?

IL: So interacting with dapps is core to what we do, but our current route is not to a browser, so we don't believe it's the best experience. If you're on iPhone you will use Chrome or Safari. And so WalletConnect is the direction we are working on where you can be on any platform, on a desktop or mobile browser, and then you just use Argent to validate transactions. We’re thinking that Argent can be your bank, and also store identity. You will use that to log in on websites, whether it's a dapp or not it doesn't matter, instead of Facebook log in. And then you will use that to confirm transactions, blockchain transactions or payments. That's the route we're taking.

We keep an eye open if that browser goes beyond the small niche it is now, then it's maybe something we'll consider, but we think the best approach is to have people to keep using Google Chrome or keep using Safari. It's not our business to build the best browser out there.

CR: What's the main thing that you think should change or that you criticize about either like just Ethereum, or blockchain, or DeFi?

IL: One criticism is we talk too much about waiting for mass adoption. We talked too much about mass adoption will come but it's really about making it happen. If you want mass adoption, you need to build a product that people will want. And that's really why we focused so much on building a simple experience that anyone can use. Let's not wait for a billion people to come. Let's get a hundred thousand, a million, 10 million by creating products people need.

CR: Why do you think everyday, non-crypto users might want to choose open finance in the future instead of traditional finance? Like what's so much better about it, do you think?

IL: I think there's a potential to be much more transparent, much more fair than the current finance. I think it's also big responsibility of people working in the space to create something better. We feel there's a strong potential to bring something completely global, completely transparent and more fair. We need to create some new services that add value to people. Right now a savings account, it's not that world changing but it's the very first step for people to get into the space.

It gets much more interesting once you can give total access to finance to an entire market that doesn't have it. So developing markets, places that don't even have a stable currency would benefit even more. And that's probably the best mission, bringing economic freedom to places in the a world that doesn't have it. I think that should be the end goal, but you know, it will take time and we are taking steps towards there.